The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

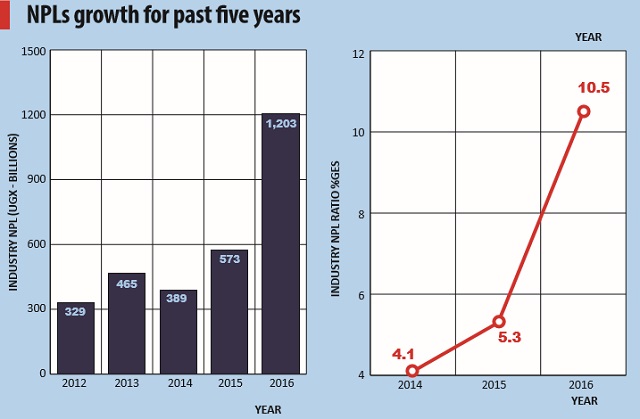

Opportunity for banks, borrowers

The move to form the ARC is being overseen by the Uganda Bankers Association (UBA). In an interview with The Independent, Wilbrod Owor; the UBA executive director and Fabian Kasi, its chairperson who also doubles as Centenary Bank managing director, said the company would assist in “either resuscitating ailing borrowers or smoothly disposing of the securities without causing undue anxiety on the part of the banks and the customers.”

They explained that with ARC in place, banking would return to lending more to corporate and private borrowers and offer more affordable rates and support economic growth.

The technical working group for the ARC has covered plenty of ground and the ARC is in very advanced stages, they said. According to UBA, which brings together 25 members, commercial banks have great interest in this process.

Setting up the ARC is based on a study PricewaterhouseCoopers (PWC) did in 2015 on behalf of UBA regarding its feasibility.

In the study, PWC undertook a detailed benchmarking study on ARCs that covered experiences from India, Malaysia, Mauritius, South Africa and Nigeria.

The ARC was earlier planned to be launched in 2016 but was delayed by the technical working group which is yet to finalise its work.

The ARC will be capitalised by its shareholders or equity partners and attract transaction funding from capital firms, investors, and other lenders. The plan is to have experts in law, asset valuation, insurance, and banking running the ARC.

The company would complement current measures implemented by banks to manage NPLs; including regular and prudent credit monitoring and restructuring of terms and conditions of the loan.

It will further provide banks whose borrowers maybe experiencing difficulties with loan repayment with relief from the stringent provisioning which would allow them to transfer such assets off their books (to the ARC) without incurring significant losses.

Borrowers on the other hand will be given an opportunity with more time to reorganise themselves so as to pay off the loans without the kind of pressure they face under the current arrangement with banks.

Owor and Kasi said the ARC would save the economy from going under in times when financial institutions and the critical sectors of the economy are affected by bad loans. Both financial institutions and private sector players thrive when business is buoyant on both sides and vice versa, they said.

No legal backing yet

Mweheire said ARCs have had mixed results in places such as India where it was introduced in 2002.

“The key lesson from these countries is that there are local nuances to be considered in implementing these solutions,” he said, “And that the government, regulators and key financial players must work very closely to find a locally relevant solution that works well for that particular economy.”

When asked to comment on the ARC, the Director of Communication at Bank of Uganda, Christine Alupo, said the business of ARC does not fall under the regulatory purview of the Financial Institutions Act that the central bank uses.

“It will become necessary to draft a separate legislation to govern the operation of asset reconstruction business in Uganda,” she told The Independent on May 10.

BoU is part of a technical committee established to oversee the implementation of the ARC.

Alupo said there are four key areas the technical working group is looking at – institution of the requisite legislation and regulation to provide the basis for oversight, completion of the incorporation process which entails putting in place the appropriate shareholding and governance structure, agreeing on the funding structure with key players, and also agreeing on the day to day operational aspects of the ARC.

A July 2016 research paper titled `ARCs – at the crossroads of making a paradigm shift in India’ published by the Associated Chambers of Commerce and Industry of India (ASSOCHAM) together with audit firm, Ernst & Young paints a bad picture about ARCs and provides some working lessons for UBA.

The paper notes in part that, whereas ARCs are good for business, they usually focus on how much of the remaining value of the distressed company can be recovered and hardly anything is done towards resolving the problems emanating from improper management.

It warns in part that these ARCs typically have low capital base and their methodology towards addressing needs of troubled companies has an overt financial focus.

The paper hints on the need for sector regulators to get more power in terms of auditing and inspection, appointments to boards, imposition of penalty for non-compliance and regulating fees charged by ARCs.

Once fairly implemented, these hints would make the ARC relevant to growing Uganda’s banking sector.

****