The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

No one deserves to die from excessive peer pressure because of failure to re-pay a micro-credit loan

COMMENT | Nathan Were |The Daily Monitor newspaper of February 02, 2019 led with a sad story of Gubindi – a resident of Jinja town in eastern Uganda who, after failure to re-pay a micro-loan of 300,000 ($81) that he obtained from Pride Microfinance Limited, took his own life in a police cell.

The story of Gubindi and many other people who are hurting silently because of unethical lending practices and brutal recovery methods by lending institutions, brings in question the intended outcomes of micro-credit and responsible lending.

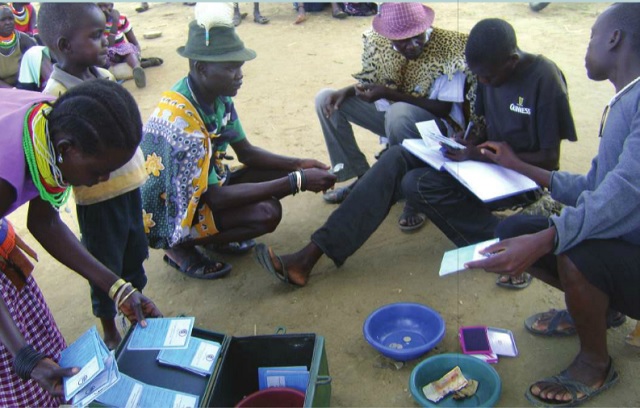

Micro-credit – mainly delivered through joint liability groups (JLG) has for many years been hailed by social impact experts as a channel through which poor households that lack collateral securities can access a micro-loan and invest in their micro and small enterprises. The industry has hailed the methodology for a near-zero default rate and many financial institutions have become profitable and rapidly grown as a result. However, repayment (or its lack thereof) presents an incomplete picture in assessing whether these joint liability loans help customers achieve original goals or even improve their financial situation.

A trail of deaths, shuttered families, broken marriages and migration out villages are just some of the many pitfalls that these group guaranteed loans continue to leave behind in the name of empowering the poor. A number of studies from around the world have consistently highlighted how excessive peer pressure from group members has caused some to flee their homes, abandon their businesses or even take their own lives.

When micro-credit was created, it’s intended outcomes were to build and not destroy lives of the poor. However, along the way, the industry has been hijacked by capitalists whose quest for profitability supersedes its original outcomes. Mohamed Yunus the Nobel peace Laurent and founder of micro-credit has continued to argue that what he founded nearly 30 years ago, has taken a completely different course. The desire to make excessive returns for shareholders is driving many institutions into unethical practices, excessive pricing, and fierce recovery methods.

It is not just about people taking their own lives, group loans are also a big inconvenience. A study conducted by one of the global financial inclusion think tanks five years ago found that people lose a lot of time and money in weekly meetings. Group borrowers are required to meet weekly, sometimes bi-weekly for several hours to discuss their loan repayment situation. For some, they must close their businesses as a result and lose income in the process. One of the clients during the same study indicated that “taking a group loan from a microfinance is like being in prison. You have no life, no privacy and no peace”.

But how did we get here? The poor have limited options when it comes to financial services. They have no collateral, no credit history or a trace of tractions to determine their cashflow. They must form groups to borrow. It is this vulnerability that micro-finance institutions are exploiting and hurting the poor in the process.

These loans are not even cheap. A recent Bank of Uganda loan pricing matrix for micro-deposit taking institutions showed that some MFIs are lending at as high as 65% effective interest rate per annum. No business can generate such returns. Infact, for many micro borrowers, these loans are eroding their working capital and slowly killing their businesses. But because they juggle many things from which they earn, it is not obvious for them to see the impact of this pricing.

Can the industry be redeemed? This remains an open question with very few answers. A few organisations have tried to advocate for responsible lending and social performance – but their efforts are not yielding the much-expected results. MFIs are at cross-roads struggling to balance the social outcomes with profitability. Some microfinance lending vehicles – the source of debt and equity funding for many MFIs – care less about social impact but concentrate on return on investment at whatever cost. The regulators are mainly concerned with financial and sound health of these institutions and less about how they treat their customers. With these contradictions, it is unlikely that we shall see microfinance return to its original intentions of empowering the poor.

*******

Mr. Were is an Access to Finance Specialist based in Nairobi.

Email: were.nathan@gmail.com