The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

Washington, United States | AFP | Florida insurance companies appear to have avoided what could have been a catastrophic hit after damage estimates from Hurricane Irma on Monday fell sharply due to last-minute shifts in the storm’s trail of destruction.

The storm spared cities on Florida’s eastern coast, which analysts said reduced the potential losses considerably.

“Our nightmare scenario did not materialize,” Shahid Hamid, director of the insurance laboratory at Florida International University’s hurricane research center, told AFP.

“The storm shifted track. Bad luck for the west coast but we’re very happy.”

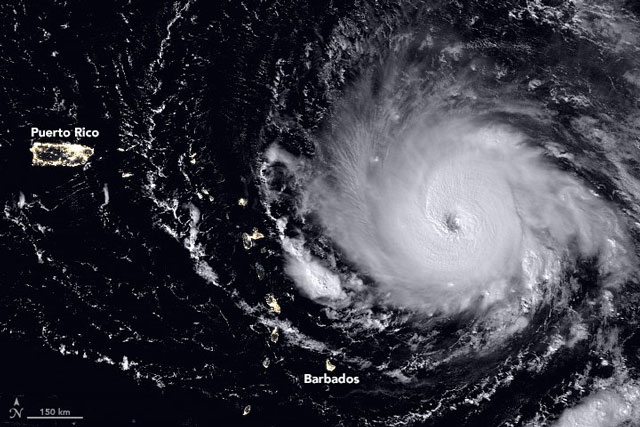

Initial models showed the storm’s path would take it over three major urban areas — Miami, West Palm Beach and Ft. Lauderdale — where residential and commercial real estate values are about $1.2 trillion.

But having strafed the Caribbean, the storm veered slightly to the west.

Hamid, who oversees stress-testing of Florida insurers to verify they can absorb the costs of the storms that routinely hit the state, said a $100 billion storm could have threatened the viability of the state’s insurers.

Damage of that magnitude raised questions about “how many insurance companies can really cope with a hurricane like Irma,” he said last week, adding that with “exceptionally high” losses, “all bets may be off” for the companies.

Financial analysis company Demotech told The Miami Herald local insurers had a total claims-paying capacity of $60 billion, so even the lower damage estimates are significant.

Catastrophe modeling firm AIR Worldwide cut its estimate of insured losses down to a range of $20 billion to $40 billion, lowering the maximum by $25 billion.

Prior to landfall, disaster modeling firm Enki Research and AccuWeather each forecast the total economic toll from Irma at $100 billion or more in the US alone.

But Enki Research founder Chuck Watson told AFP on Monday his latest economic damage estimate had dropped to $50 billion: “Not as bad as it could have been but bad enough.”

RELATED VIDEO: